On Monday, January 28, OrMu’s Minister of Finance and Public Credit, Ivan Acosta, presented a proposal to reform Nicaragua’s tax code to the National Assembly. Armed with a seizure-inducing powerpoint slide deck, Mr. Acosta informed the Assembly that the reforms were necessary to “Protect employment, economic growth, welfare and social security of Nicaraguan families.”

Reforma-LCT-28Ene19Here are some of main points of the measure, as summarized in the presentation:

- The reform anticipates tax revenues of C$10,168.6 for the fiscal year of 2019 (about $300 million). By 2022, tax revenues would reach C$16,004.5 (about $490 million) (p, 59).

- Income tax rates for businesses earning between C$ 60 and C$160 million per year increase from 1% to 2% or 3%, depending on business size. Small business income will continue to be taxed at 1%. Taxes are paid monthly. If by the end of the fiscal year it turns out that a business has overpaid, the excess amount can be applied to next year’s taxes, and the government will issue bonds that can be sold in the stock market. However, the government will only issue such bonds until 2021 (p. 40)

- Exporters can only deduct the export duties (1.5%) from their income tax if it turns out that they have overpaid (p. 41).

- The tax on services by foreign providers (e.g., consultants, lawyers, firms, etc, who are non-residents) increases from 15% to 25% (p. 41).

- Taxes on stipends and/or any kind of monetary allowance received for serving on a board of directors increase from 12.5% to 25%. If the person serving on the board is a foreign national, the tax increases from 15% to 25% (p. 38)

- New tax brackets for goods that must be registered (e.g., properties or vehicles). If the property’s worth is assessed somewhere between U$300.01 to $400 thousand, the owner must pay a 5% tax. For properties worth between $400.01 and 500 thousand, the tax is 6%, and for properties worth over $500 thousands, it is 7% (p. 41)

- Tax on investment funds and trusts increases from 10% to 15% (p. 41).

- Casinos must now pay $50 per slot machine and $600 per table. Prior to the reform, Casinos paid a $25 fee for each of the first 100 machines, $35 for the next 200, and $50 for the next 300 or more. In addition, Casinos paid $400 per gambling table.

- Through a modification of Law 387 — Law of Exploration and Exploitation of Mines — the royalties mines pay to the government to extract gold and silver will increase from 3% to 5%. In addition, these royalties cannot be deducted from the overall income tax at the end of the fiscal year (p. 44).

- The Value Added Tax (VAT) will be applied to several manufactured products, including products that are part of the “canasta basica” — goods that are routinely purchased by households — such as laundry soap, toilet paper, matches, sanitary napkins, and toothbrushes. These products are typically imported and/or produced by large manufacturers, whose economic activities are explicitly excluded from tax exemption. Only products that “come directly from small agricultural producers, from micro and/or small industrial enterprises, or artisanal fisheries” are exempt from paying the VAT (p. 46).

- Purchases made at a municipal market are explicitly exempted from the VAT. In other words, if you buy a shirt at a small stand in the municipal market you will not pay the VAT, but if you buy the same shirt the mall, you will pay it (P. 46). The same reasoning applies to buying groceries at the municipal market vs. buying them at the supermarket.

- The sin tax on tobacco products will increase progressively between 2019 and 2021. For example, the sin tax on cigarettes goes from C$2,000 per thousand units in 2019, to C$ 3450 per thousand units by 2021. In addition, sin taxes on alcoholic beverages will be C$50.00 per liter; the sin tax on sugary drinks will increase from 9% to 15%, and the sin tax for foods with low nutritional value increased by 5%.

The proposed tax reform also includes a number of exemptions for basic staples, including corn, wheat, red and black beans, tomatoes, white and yellow onions, peppers, cabbage, potatoes, bananas, plantains, and rice, as long as it is 80/20 quality or lower. Also exempted are live chickens, eggs, corn tortillas, pinol and pinolillo, traditional bread, wheat flour, soy flour, and corn flour.

According to Julio Francisco Baez Cortes, one of Nicaragua’s leading tax expert and founder of Baez Cortes and Associates, the proposed changes exempt products that have been tax exempted for many years. “It reaches the extreme of […] exonerating chicken gizzards, beans, tortilas, and pinolillo”

Continuación: b) anuncian exoneraciones de productos de consumo popular que ya estaban exonerados desde hace 15, 20 y hasta 30 años, llegándose al extremo de esta pobreza técnica al "exonerar" "¡chicaca de pollo, frijol, tortilla y pinolillo!"

— Julio Francisco Báez Cortés (@kikobaezc) January 28, 2019

The OrMu administration has been framing the proposal as a matter of “fairness”, whereby the rich pay more and that revenue can be used to support social programs and public investment to benefit the poor. However, the tax increases, which are by no means gradual, will increase the costs of production. In addition, new and/or updated duties on equipment, parts, and other supplies needed for large-scale agricultural and industrial production increase production costs even further. This scenario is what the Nicaraguan capital, represented COSEP, forecasts once the reform passes

La propuesta de reforma a la Ley de Concertación Tributaria pretende gravar con impuestos casi todos los bienes agrícolas y el ganado en pie; lo que provocaría un aumento indirecto en el costo de la mayoría de productos alimenticios de la canasta básica. pic.twitter.com/7p6C1MQn86

— COSEP Nicaragua (@COSEPNicaragua) February 1, 2019

In other words, even though OrMu spokespersons like Assemblyman Walmaro Gutierrez have said that “all basic staples will be tax exempt”, prices will still increase because producers will shift the economic costs onto the consumer, unless the Ortega-Murillo government resorts to subsidies to stimulate production and/or offset increased consumer prices, like the Sandinistas did in the 1980s (for an overview of 1980s Macroeconomic Policy, see Ocampo, 1991).

According to Gisella Canales, a financial blogger, it is a folly to think that only certain groups of people will be affected by the tax reform. In a twitter thread, she explains that everyone will be affected.

No one can afford to think that the reforms will only affect certain groups of people. They will affect everyone. The difference is that not everyone has pockets deep enough to be able to manage [the new costs]. A greater decrease in consumption pushes us all towards economic depression. Be warned!

If you use soap to wash your clothes and for bathing, if you buy detergent, brush your teeth with toothpaste, use deodorant, among other BASIC things, you better get your pocketbook ready.

Nicaragua does not produce enough onions to cover national demand, which is why we import [onions[. Now, those onions (which are usually cheaper than locally-grown onions) will go up in price […]

And to that, you have to add the effect of the increase of employer contributions to social security, which goes from 19% to 21.5% o 22.5%, depending on business size.

If medium-sized farm that produces eggs employs 55 workers and pays them an average salary of C$10,000, [that farm] paid C$1,900 per employee, per month to INSS, for a total of C$104,500. After the reform, they will pay C$2,250 per employee, for a total of C$123,750. Do you really think the price of those eggs won’t go up?

Tax Reform Impact on Consumers

Price increases and more taxes are problematic, but perhaps the most controversial move made in the proposal was the attempt on taxing remittances. According to the World Bank, personal remittances were approximately 10% of the GDP in 2017. In addition, Nicaragua’s Central Bank’s numbers indicate that remittance’s contribution to the GDP increases yearly.

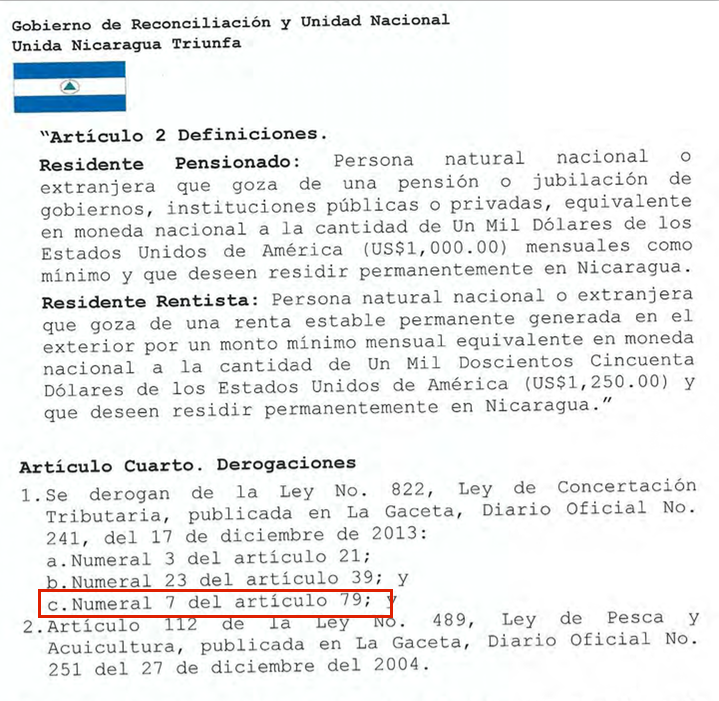

The Assembly circulated the proposal via its website. Originally, the document axed paragraph 7 of Article 79 of the tax code, which established tax exemption for remittances. This decision received ample media coverage, and outraged many Nicaraguans who took to social media to express their rejection. It did not take long for OrMu government to backtrack and delete the text from the proposal.

In order to reassure the public, the OrMu government opted to accuse the Nicaraguan independent media of peddling fake news. For example, Walmaro Gutierrez said in a press conference attended only by Orteguista media that fake news about remittances was an attempt at manipulating the public:

Minister Ivan Acosta was even more categorical in his characterization. Mr. Acosta stated that anyone who suggested taxing remittances was perverse.

Only a perverse mind that has said many lies could think that [we] are planning to tax the remittances that our families receive from their relatives. We have never said that. We have never said it in the past, nor are we saying it now, because those are resources that the families who live abroad send to support Nicaraguan families. [Taxing remittances] would be a great injustice; it would be grotesque, and only perverse minds would think that, probably because that is what they would do if they were in power.

El ministro de Hacienda y Crédito Público, Iván Acosta, destaca que nunca se ha mencionado a gravar las remesas pic.twitter.com/VKa1FWT2dn

— El 19 Digital (@el19digital) January 29, 2019

Unfortunately, by then many people, myself included, had downloaded the original draft from the Assembly’s website. Article 4 of the proposal deals with “derogations”, and it did, in fact, strike down the tax exempt status for remittances.

Original draft of OrMu Government’s tax reform proposal

The tax reform bill was scheduled for discussion on Friday, Feb 1. The debate was postponed without explanation and has yet to be rescheduled. With an Ortega-controlled Assembly, the law is certain to pass.

Related Posts

Propaganda Goals Hamper Risk Communication in Nicaragua.

Propaganda Goals Hamper Risk Communication in Nicaragua.- Nicaragua: MINSA’s Muddled Briefings Underplay COVID-19 Impact in Nicaragua.

PAHO Director: “We see Inadequate Prevention and Control” of COVID19 in Nicaragua

PAHO Director: “We see Inadequate Prevention and Control” of COVID19 in Nicaragua #Nicaragua: Bishop Álvarez Announces #COVID19 Project for Diocese of Matagalpa; MINSA Quashes Idea

#Nicaragua: Bishop Álvarez Announces #COVID19 Project for Diocese of Matagalpa; MINSA Quashes Idea Nicaragua: COVID-19 Response Marred by Inconsistencies, Recklessness, and an Absentee President

Nicaragua: COVID-19 Response Marred by Inconsistencies, Recklessness, and an Absentee President- Nicaragua’s COVID-19 Health Communication: An Exercise in Doublespeak.